Where do corporate earnings actually come from?

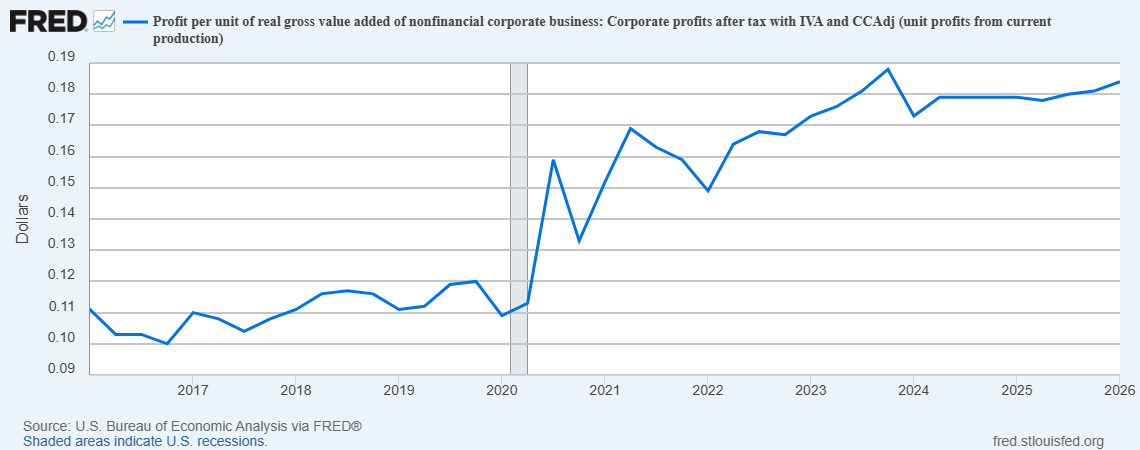

For years it seems, the broad story has been that corporate profit margins are expanding and earnings are growing. But where do those earnings come from? The answer has important ramifications for thinking about economic cycles and market returns, that might affect your portfolio.

Source: St. Louis Federal Reserve Board, 6/22/2026

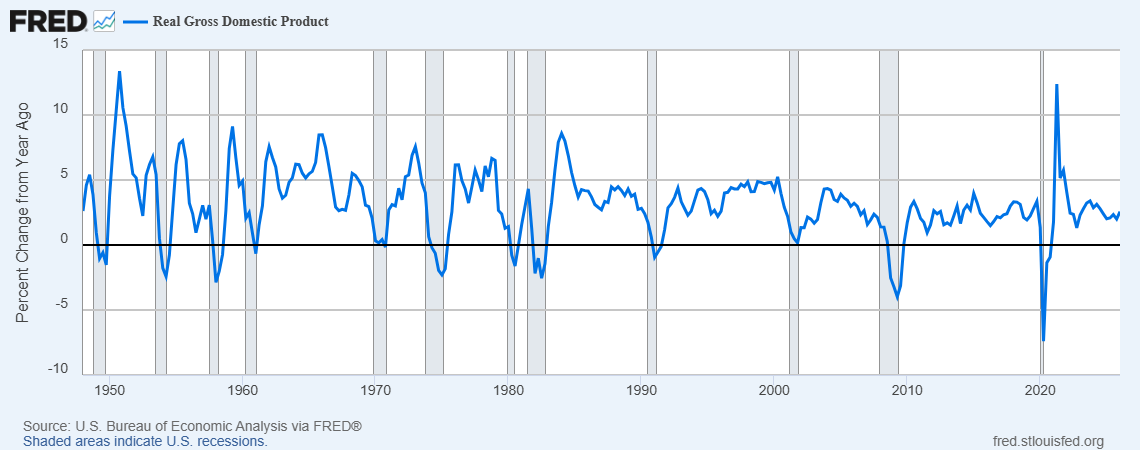

I find it helpful to think of GDP as a pie, and different actors get a larger or smaller slice of the pie at times. The pie does grow as businesses convert natural resources into useful goods, technology improves productivity, or government increases spending and debt. U.S GDP growth has averaged around 2.5%.

Source: St. Louis Federal Reserve Board, 6/22/2026

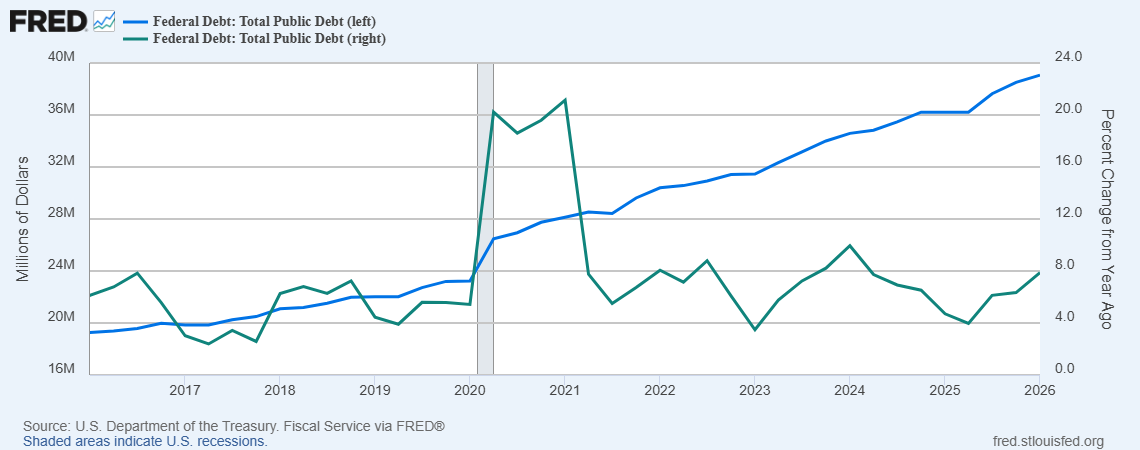

This idea is known as the Kalecki profit equation, Corporate Profits = Investment – Household Saving + Government Deficits + the Trade Balance. In recent years, government debt has increased and personal savings has dropped.

Source: St. Louis Federal Reserve Board, 6/22/2026

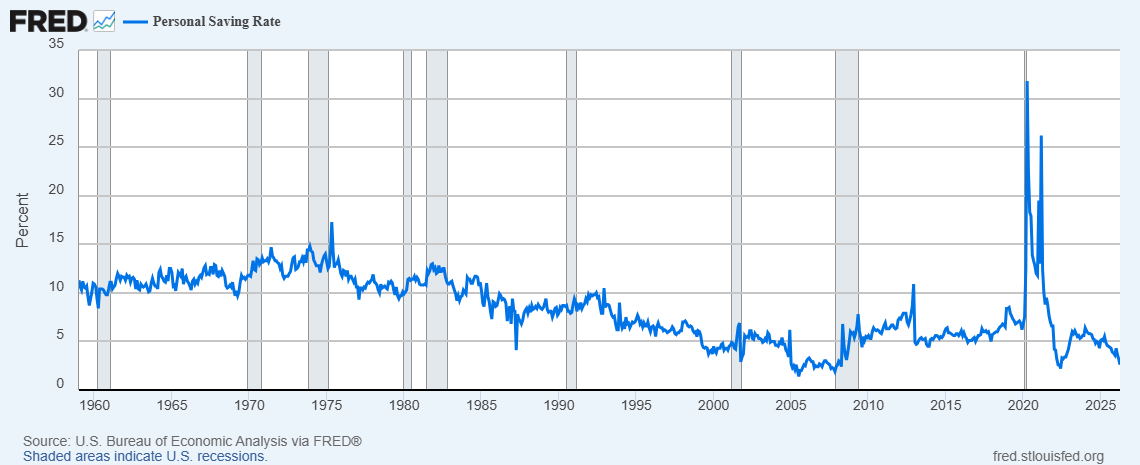

Source: St. Louis Federal Reserve Board, 6/22/2026

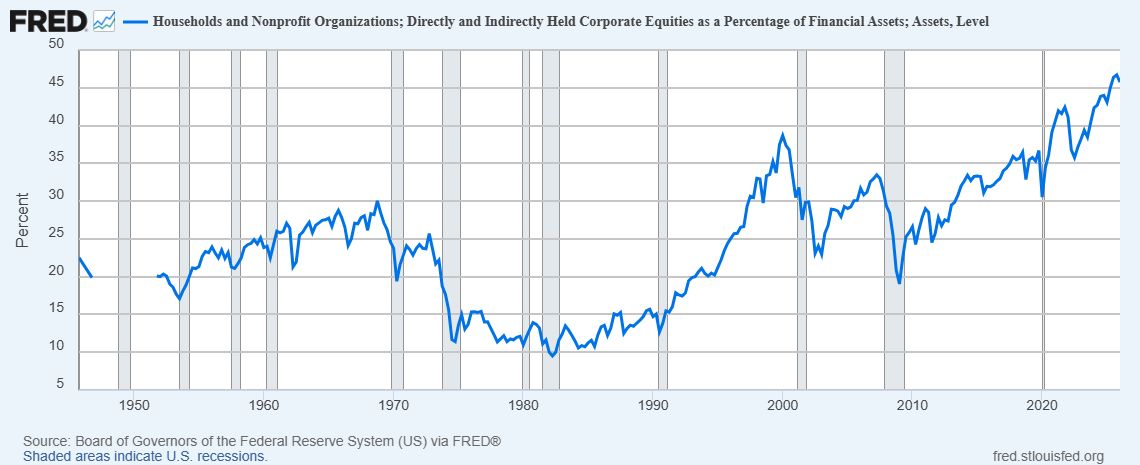

Is it any wonder that corporate profits, and therefore the market, are higher? Not only that, but the household allocation to stocks has risen as a percentage of household wealth. The market is influenced by supply and demand, like other goods. If there is more demand for equities, investors will be willing to pay a higher price for them, pushing valuation ratios like price-to-earnings higher. If households are allocating more of their savings to equities, this could push valuations higher, and we have seen exactly this over the last five years.

Source: St. Louis Federal Reserve Board, 6/22/2026

Within businesses, the pie gets divided again. When one sector is earning outsized profits, that is generally at the expense of some other sectors. For example, if the price of oil and gasoline rises, the oil producers will have higher profits, and consumers may pull back on other discretionary purchases like travel or going out to eat. And the question becomes, how long will this last? When you think in these terms, some things start to make sense.

For much of the last 10+ years the main winners were the “Mag 7”. The largest companies today are a) immensely profitable and b) benefit the most from new assets flowing into equities (when someone uses new money to buy an index fund, say, from a paycheck or funds that were allocated to bonds or in cash, the index fund buys all the stocks in the index according to their market cap, so the fund must buy more of the biggest companies[1]). Their piece of the pie probably came from other forms of advertising and from consumers who bought more products. Now, those same companies are sending much of their profits to chip designers and manufacturers. The question, again, is for how long?

When these changes in the flow of profits occur, the market sometimes prices these flows as if they’ll never end. The new norm is assumed to continue indefinitely. As investors chase the profits, they push up the valuations and future expectations for these companies. Ultimately when the flows do change again, the last investors in often end up with poor returns historically.

The important lesson of the earnings pie, is that “earnings” do not come out of thin air. There’s a somewhat fixed pool of assets that are traded between consumers and businesses, and when one side increases it is generally at the expense of the other. Currently, corporate profits have been strong, and consumer savings have been low, and households are allocating more of their savings to equities. It’s important to consider that historically these cycles tend to reverse eventually.

I want to be clear that this is not a market timing call. This is not to cause fear or encourage making decisions out of panic. That said, it is good to review your plan and consider what would happen if future returns are lower, to review your portfolio and see if it well diversified across sectors, company sizes, and geographies. We tend to feel more comfortable investing in assets that have recently gone up in value, even if that means future returns are likely lower and risk might actually be higher. If your portfolio reflects this recency bias, it might be time to rebalance or reallocate.

This post is for educational purposes only and does not constitute personalized investment advice. Past performance is not indicative of future results. Planalto Financial LLC is a registered investment adviser in the state of Alabama.

[1] Some people say that index funds are increasing the “momentum” effect in markets, because they allegedly buy more of stocks that are going up in price. I think this is not precisely true. If no one was adding or removing assets from index funds, they would not be buying or selling much of anything. Companies are added and removed from the index occasionally, but they don’t have to buy more just because the stock price went up, or sell because it went down. However, as people add new money to the index fund the fund WILL have to buy shares of the companies in the index, and the fund will buy proportionally more of the largest companies. This is why the increase in the household allocation to equities is relevant, this is one measure of new money into equities, though not limited to index funds.